With the sticker price at some colleges now topping $50,000 a year, it’s no wonder so many parents are worried about how they will afford their teenager’s tuition bill.

But here’s the good news. Most students don’t pay anywhere near the sticker price for their college education. In fact, today, the average student at a private, four-year college pays only about half that price, according to a recent survey by the National Association of College and University Business Officers.

“The sticker price is just like a sticker price for a car. What you see on the windshield is not necessarily what you are going to pay,” says Rob Kron, head of Investment and Retirement Education for BlackRock, an investment management firm based in New York City. “A student’s unique situation and the schools they are applying to will determine how much of a discount they will receive.”

Making College Affordable

So, how can you ensure your student doesn’t pay sticker price for his college education, especially if you’re a higher-income household? The first step is to acquaint yourself with the two kinds of financial aid colleges offer, namely merit aid and need-based aid.

Merit aid is money awarded to applicants based on merit, typically a strong academic performance in high school. Need-based aid is awarded to applicants based on financial need and is mostly determined by household income. Students in households with higher incomes won’t qualify for much, if any, need-based aid. But they can qualify for merit aid.

Do Your Homework

Note that how much need-based and merit aid colleges offer differs from one institution to the next. Some offer no merit aid—that includes the Ivies and many other top-tier institutions—while others offer a lot of merit aid. Same for need-based aid. Some institutions will meet 100 percent of need, while others meet a much lower percentage.

As your teenager decides which colleges to apply to, it’s important to make sure those colleges will offer your teenager the kind of aid (merit or need-based) that will discount your tuition bill, says BlackRock’s Kron. You can determine what kind of aid your teenager will likely receive from a particular college with what’s called a Net Price Calculator.

“The federal government mandates that any school that receives federal funding has a Net Price Calculator on its website,” explains Kron. “You provide information about yourself and your student. The Net Price Calculator will show you what the average fees, room and board, transportation, and personal expenses are for students like yours at that school. That gives you an idea of your total cost of attendance.”

This is an approximation of what your student is likely to pay to attend that school. You won’t know for sure that this will make college affordable until your teenager gets in and receives his or her official financial aid package.

“But it gives you a cost you can start to plan around,” explains Kron. “And if you don’t complete this exercise before submitting the application, you may find, you didn’t apply anywhere that you can actually afford to go.”

Be Careful of Debt

Even with discounts, most families will still have a tuition bill to pay. And let’s face it. Even if your teenager scores the average 50-or-so percent discount, that can still leave you on the hook for $20,000 to $30,000 a year at a private four-year college.

“You have to be realistic about what you can do as a family,” Kron says. “Right up front, as you go through the process of putting schools on this list, you talk about the chance of getting in, as well as the chance of being able to pay for it.”

That includes what you (parents) can afford to pay toward tuition (from savings and income), as well as the amount of debt (student loans) your teenager should take on. Be cautious about allowing your teenager to assume more debt than she can comfortably repay after graduation.

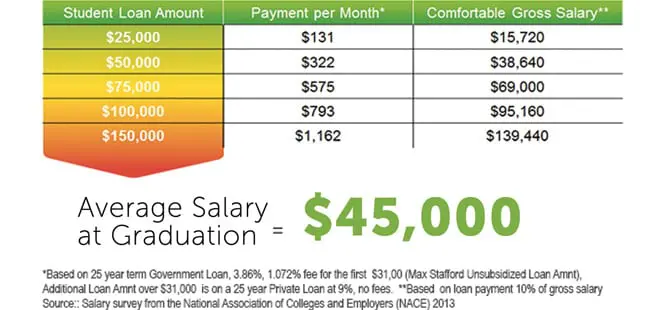

“If you look at the average starting salary, which is around $45,000, how much debt is manageable? A general rule is that you don’t want to have more than 10 percent of your monthly income taken up by a student loan payment,” explains Kron. For $45,000, that 10 percent is around $300 a month (or around $50,000 in student loan debt).

Managing Student Debt

Meanwhile, if your teenager is passionate about a career in a field with lower entry-level salaries—say teaching—or plans to pursue a costly graduate degree—say medicine or law—then your teenager’s debt will need to be that much lower at graduation (see chart below).

“You can’t really know what your teenager is going to make coming out of college. So why would you want to set them up for an unsustainable debt burden?” Kron advises.

Parents should also be cautious about borrowing, particularly if repayments will interfere with your ability to save for retirement.

Consider loan options carefully, especially when it comes to private loans. Students should always maximize the federal government’s loan offerings before considering private loans. The government has several low-interest loan programs for students and parents — including Stafford Loans and Parent Plus LOANS. Private lenders are not required to keep interest rates for educational loans low (and often do not).

Even Modest Savings Help

So far we’ve covered two sources of paying for college: merit and need-based aid and student loans. The last piece of the puzzle is savings.

To be sure, saving for a college education can feel overwhelming. Even with aid, it’s a lot of money.

But, stresses Kron, even modest amounts of savings can help in affording college. “Every dollar you save, regardless of when you start saving, is creating that much more opportunity for your child. It’s allowing one more school to be on that affordable list. It’s one more career decision that wasn’t influenced by, ‘Oh, I’ve got to make a certain amount of money to service this debt.’”

Approach savings by taking into account the years until your teenager goes to college, as well as the four or five years he or she will be a student. “Say you’ve got a freshman in high school and you haven’t saved anything for them. It’s not game over,” notes Kron. “It’s four years before they get to school and four years while they are in school. That’s eight years.”

College Savings Plans

Among the most popular ways to save for college is what’s called a 529 plan. Think of it as an IRA for your teenager’s education. Money you put into a 529 grows tax-free. And if you use the money saved in a 529 plan for a qualified education expense, those withdrawals are tax-free too. Qualified expenses include tuition, room and board, and even books and other supplies.

“Say you save $5,000 in this account. While the money remains in the account, you don’t have to pay taxes on interest you earn from the account. But if that $5,000 was sitting in any other type of account, you would have to pay taxes on earnings,” explains Kron.

Some parents worry that saving for college will penalize them when it comes to getting financial aid from a college. Not true, adds Kron. “Parents should keep in mind that the largest component of the financial aid formula is parents’ income. For the most part, that is what’s going to determine whether or not they will qualify for need-based financial aid.”